5 Stablecoins for 2026: Navigating the New Regulatory Landscape and Yield Opportunities

The 2026 stablecoin landscape is defined by strict reserve audits and yield-bearing compliance, shifting focus from pure speculation to regulated utility. We evaluated five assets that meet new legislative requirements while offering transparent, on-chain yield opportunities.

Pick the right fit

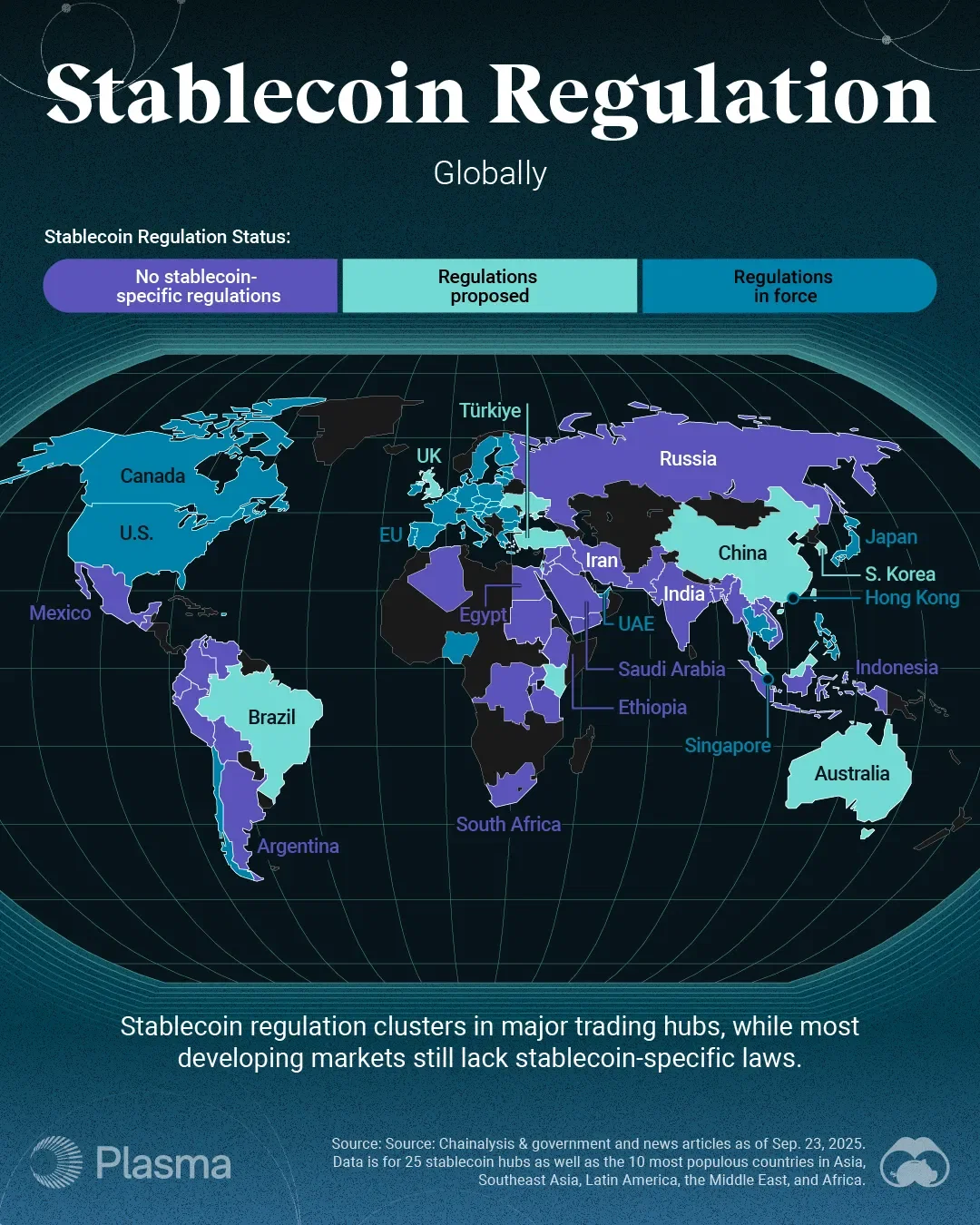

Choosing a stablecoin in 2026 is no longer just about picking the biggest name. With the GENIUS Act now defining the regulatory floor, the market has split into clear tiers of safety and utility. Your choice depends on whether you prioritize strict regulatory compliance or specific yield features.

The GENIUS Act requires permitted issuers to back reserves on a one-to-one basis with approved assets like US dollars or federal reserve notes. Before allocating capital, check if the issuer is listed as a permitted entity under the new framework. This verification protects you from regulatory friction and ensures your assets are legally backed.

Look for issuers that publish real-time or frequent attestations of their reserve composition. A transparent ledger allows you to see exactly what backs your stablecoin. Avoid projects that rely on opaque commercial paper or complex derivatives, as these introduce counterparty risk that the new regulations aim to eliminate.

Some stablecoins now offer yield by investing reserves in short-term Treasuries or regulated money market funds. Compare these yields against the issuer's fee structure. Remember that yield often comes with higher minimum holding periods or specific jurisdictional restrictions. Ensure the yield source is compliant with the GENIUS Act's asset restrictions.

In 2026, stablecoins are becoming a global payment rail for remittances and B2B settlements. If you need to move funds across borders, choose a stablecoin with wide exchange support and low withdrawal fees. Test the liquidity on your target exchanges to ensure you can exit your position quickly without significant slippage.

Even with regulatory backing, technical risk remains. Prioritize stablecoins that have undergone multiple independent security audits and have bug bounty programs. Look for issuers that use multi-signature wallets for treasury management and have clear incident response protocols in place.

| Feature | Regulatory Compliance | Yield Potential | Liquidity |

|---|---|---|---|

| Tier 1 (Compliant) | High (GENIUS Act) | Low to Moderate | High |

| Tier 2 (Yield-Focused) | Moderate (Varies) | High | Moderate |

| Tier 3 (Niche) | Low (Unverified) | Variable | Low |

As an Amazon Associate, we may earn from qualifying purchases.

FAQ: Stablecoin Regulations and 2026 Trends

Stablecoins have moved from experimental crypto assets to regulated financial infrastructure. The 2026 landscape is defined by new federal rules and shifting use cases. Here are answers to the most common questions about the current regulatory environment and market direction.

No comments yet. Be the first to share your thoughts!