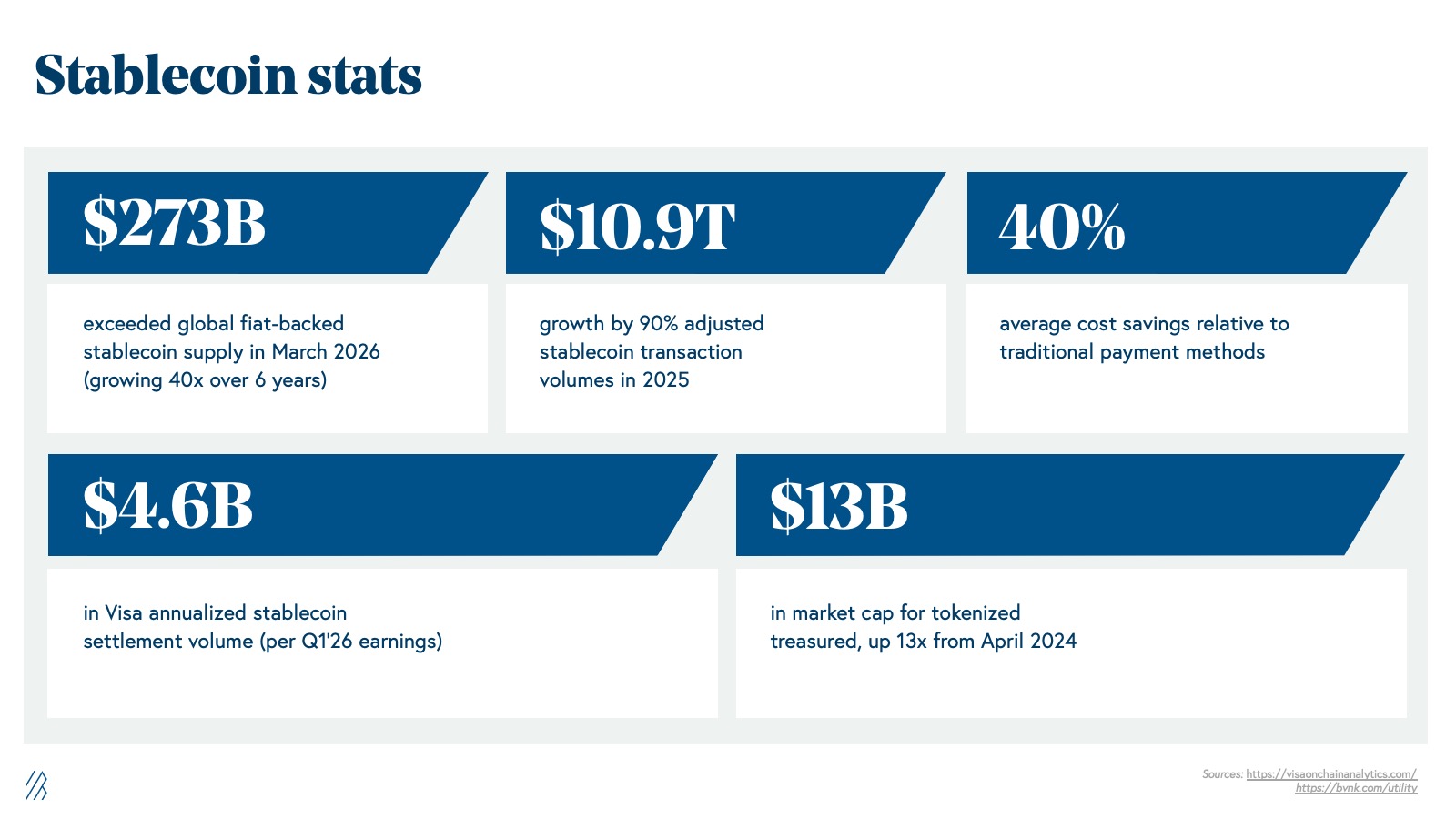

Regulatory clarity reshapes stablecoin demand

The GENIUS Act, enacted on July 18, 2025, established a definitive federal framework for payment stablecoin activities, replacing years of regulatory ambiguity with a structured compliance environment [src-serp-2]. This legislative foundation, supported by proposed rules from the Office of the Comptroller of the Currency (OCC), Treasury, and NCUA, has created a predictable landscape for digital asset issuers. The clarity provided by these regulations is not merely procedural; it is a primary driver of institutional adoption and market expansion.

Federal Register data indicates that this regulatory certainty is fueling rapid issuance growth. Forecasts project that payment stablecoin issuance will reach $250 billion in 2025, climbing to an upper bound of $500 billion by 2026 [src-serp-1]. This trajectory suggests that compliant issuers are positioned to capture the majority of this growth, as traditional financial institutions and payment providers migrate toward regulated digital currencies to meet demand for efficient settlement and yield-bearing assets.

Established issuers like USDC and PYUSD are leveraging this environment to solidify their market positions. The GENIUS Act’s requirements for transparency, reserve backing, and redemption capabilities—such as the mandated two-day redemption window—favor entities with robust compliance infrastructure. As global rules accelerate adoption and reshape payment systems [src-serp-7], these compliant stablecoins are becoming integral to the broader financial infrastructure, bridging the gap between traditional banking and digital innovation.

The chart above illustrates the market trajectory of USDC, reflecting the broader trend of stablecoin adoption under the new regulatory regime. As issuers comply with the GENIUS Act’s requirements, the concentration of market share among compliant players is expected to increase, reinforcing the dominance of established names in the 2026 stablecoin landscape.

How USDC and PYUSD Meet New Compliance Standards

The GENIUS Act establishes a rigorous federal framework for payment stablecoins, requiring issuers to maintain high liquidity, provide transparent reserves, and partner with regulated banking institutions. Under proposed rules from the FDIC and Treasury, payment stablecoin issuers must redeem tokens within two business days [src-serp-5]. This mandate shifts the competitive advantage toward issuers with established banking partnerships and institutional-grade reserve management.

Circle and PayPal have positioned their respective tokens, USDC and PYUSD, to align directly with these regulatory requirements. Both issuers prioritize full reserve backing and regulatory transparency to mitigate counterparty risk. The following comparison outlines how each project satisfies the core compliance pillars of the new regime.

| Compliance Feature | USDC (Circle) | PYUSD (PayPal) |

|---|---|---|

| Issuer Type | Financial Infrastructure | Fintech Payment Platform |

| Reserve Composition | Cash & Short-Term Treasuries | Cash & Short-Term Treasuries |

| Redemption Speed | Same-Day / 2 Business Days | Same-Day / 2 Business Days |

| Primary Banking Partners | State & National Banks | Major U.S. Commercial Banks |

Circle operates as specialized financial infrastructure, leveraging its long-standing relationships with state and national banks to ensure seamless fiat on-ramps and off-ramps. This structure supports the two-business-day redemption window mandated by the FDIC’s proposed rule [src-serp-5]. USDC’s reserves are audited monthly, providing the transparency required by the Treasury’s implementation of the GENIUS Act [src-serp-3].

PayPal utilizes its massive existing user base and established banking relationships to launch PYUSD. By integrating PYUSD directly into its payment ecosystem, PayPal ensures that redemption requests are processed through familiar, regulated channels. This approach reduces friction for consumers while satisfying the requirement for payment stablecoin issuers to operate within the traditional banking framework [src-serp-6].

The convergence of these two models highlights a broader industry shift: stability is no longer just a technical feature but a regulatory necessity. Issuers that can prove liquidity and compliance will capture the majority of the estimated $500 billion market forecast for regulated stablecoins. The NCUA’s parallel proposals further reinforce this trend, signaling that only issuers with robust compliance infrastructure will survive the 2026 regulatory landscape [src-serp-4].

Banking Integration and Redemption Rules

The proposed GENIUS Act fundamentally alters the operational backbone of stablecoin issuers by mandating strict banking integration. Under the new framework, Payment-Product Stablecoin Issuers (PPSIs) must maintain deep liquidity reserves within regulated U.S. banks to ensure immediate access to funds. This requirement shifts the liability structure away from opaque commercial paper or private credit, forcing issuers to rely on the traditional banking safety net. As noted by the FDIC, this move is designed to eliminate the settlement risk that plagued earlier digital asset models, ensuring that stablecoin liabilities are backed by tangible, bank-held assets rather than speculative instruments.

At the core of this integration is the two-business-day redemption mandate. The proposed rule requires PPSIs to redeem a payment stablecoin within two business days of a holder’s request. This timeline mirrors the standard ACH settlement window, effectively aligning stablecoin withdrawals with the existing U.S. payments infrastructure. While this may seem redundant for on-chain transactions, it is critical for institutional off-ramping and large-scale corporate settlements. Issuers must now build robust banking corridors that can handle peak redemption volumes without delaying payouts, a significant departure from the "withdrawal freezes" seen during previous market stress events.

To comply with these rules, issuers like Circle (USDC) and PayPal (PYUSD) are restructuring their reserve management strategies. They are moving away from diversified money market funds toward direct banking relationships that offer greater transparency and regulatory clarity. This shift not only increases operational costs but also raises the barrier to entry for new stablecoin providers. The result is a consolidation of market power among established players who can afford the necessary banking infrastructure and compliance overhead. As the GENIUS Act moves through the legislative process, the stability of the $500 billion stablecoin market will increasingly depend on the health of these banking partnerships.

Market consolidation favors top issuers

The regulatory framework established by the GENIUS Act, enacted on July 18, 2025, has created a bifurcated market where compliance is no longer optional but a prerequisite for survival. As the Office of the Comptroller of the Currency (OCC) finalizes its proposed rulemaking, the cost of meeting reserve transparency and redemption standards has become a barrier to entry that smaller issuers cannot easily absorb [src-serp-2]. This shift is accelerating a natural consolidation, pushing the market toward a duopoly of USDC and PYUSD as the primary compliant rails.

Industry analysis suggests that stablecoin adoption will continue to grow, with forecasts pointing toward a $500 billion market cap as these assets integrate into traditional payment infrastructure [src-serp-7]. However, this growth is not evenly distributed. The requirement for immediate, two-day redemption capabilities and strict reserve auditing means that only issuers with significant scale and institutional backing can maintain the necessary operational margins. Smaller or non-compliant stablecoins are likely to exit the market or merge with larger entities, concentrating liquidity and trust in the leading platforms.

For merchants and developers, this consolidation simplifies the technical landscape. By relying on USDC and PYUSD, businesses can comply with the new rules with confidence, knowing these issuers are positioned to meet the stringent requirements of the 2026 regulatory environment. The strategic implication is clear: compliance is the new competitive advantage, and the market is rewarding those who can deliver it at scale.

No comments yet. Be the first to share your thoughts!